10 Principles of Economics - Implementation in My Life

More information

When we talk about a list of economic principles, this most commonly refers to Gregory Mankiw’s “Ten Principles of Economics.” The list is a set of principles about the way economics should work. The 10 principles are divided into three categories: decisions people make, the work of the economy as a whole and people interactions. 10 principles of economy is the very basic principle that can be applied in our daily life from all ages, even for stude

Chapter 1 - The Ten Principles of Economics

thumb|300px|right

The Ten Principles Of Economics [ ]

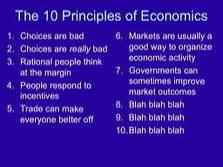

Principle 1: People face trade-offs.

Principle 2: The cost of something is what you give up to get it.

Principle 3: Rational people think at the margin.

Principle 4: People respond to incentives.

Principle 5: Trade can make everyone better off.

Principle 6: Markets are usually a good way to organize economic activity.

Principle 7: Governments can sometimes improve market outcomes.

Principle 8: A country's standard of living depends on its ability to produce goods and services.

Principle 9: Prices rise when the government prints too much money.

Principle 10: Society faces a short-run trade-off between inflation and unemployment.

Vocabulary [ ]

Scarcity

Definition: The limited nature of society's resources.

What It Means:

Economics

Definition: The study of how society manages its scarce resources.

What It Means:

Efficiency

Definition: The property of society getting the most it can from its scarce resources.

What It Means:

Equality

Definition: The property of distributing economic prosperity uniformly among the members of society.

What It Means:

Opportunity Cost

Definition: Whatever must be given up to obtain some item.

What It Means:

Rational People

Definition: People who systematically and purposefully do the best they can to achieve their objectives.

What It Means:

Marginal Changes

Definition: Small incremental adjustments to a plan of action.

What It Means:

Incentive

Definition: Something that induces a person to act.

What It Means:

Market Economy

Definition: An economy that allocates resources through the decentralized decisions of many firms and households as they interact in markets for goods and services.

What It Means:

Property Rights

Definition: The ability of an individual to own and exercise control over scarce resources.

What It Means:

Market Failure

Definition: A situation in which a market left on its own fails to allocate resources efficiently.

What It Means:

Externality

Definition: The impact of one person's actions on the well-being of a bystander.

What It Means:

Market Power

Definition: The ability of a single economic actor (or small group of actors) to have a substantial influence on market prices.

What It Means:

Productivity

Definition: The quantity of goods and services produced from each unit of labor input.

What It Means:

Inflation

Definition: An increase in the overall level of prices in the economy.

What It Means:

Business Cycle

Definition: Fluctuations in economic activity, such as employment and production.

5 Economic concepts you need to know

An understanding of these concepts will equip you with vital tools for your own decision making

Economics, at its simplest, is a study of how and why choices are made. An understanding of economics provides you with vital tools for your own decision making. Here are five key concepts that form the basis of all economics.

1. Scarcity

Look around and you will realise that there is a gap between the resources available and the wants that need to be satisfied. This gap between limited or scarce resources and theoretically unlimited wants is called scarcity. This forces people to allocate resources in a manner that all basic needs are satisfied and as much of the wants are fulfilled as possible.

For example, when you enter a metro train on your way to office/ school, the number of seats available is limited. But the number of passengers who enter the metro are much higher. This raises the question of how to allocate these seats. One way is to let each passenger find a seat based on his abilities. The other is to reserve some seats for some passengers – like reserving some seats for senior citizens. Another solution could be to limit the demand by only allowing a limited number of people enter the metro.

2. Competition

Scarcity leads to competition. The Samuel Johnson Dictionary defined it as “the act of endeavouring to gain what another endeavours to gain at the same time”. You would be familiar with this already – through childhood games, sporting events, trying to get a seat in the metro, finding a job are all competitions. All modern economies are built on the concept of competition, and the fact that different entities end up with different scare resources. One way of ensuring favourable outcomes for society as a whole in such a scenario is the market system.

3. Demand & supply

Given the scarcity of resources, no human being can be self-sufficient. So, they produce something and “supply” it to their fellow humans. In return, they take something from them to fulfil their own “demands”. This, of course, is trade. In simple terms, supply is how much of something is available in the market and demand is how much of it the people want. One way these are related is through price.

Generally speaking, if the demand for something increases faster than the supply – the price will go up. This is because the supplier realizes that more money can be made from whatever he/she is supplying. Price acts as a mechanism for filtering out demand. Imagine going out to shop for mangoes, if the price were as high as ₹1000 per kg – you would most likely not demand those, and the demand will get limited to people who can afford such a price. On the other hand, if the price is lowered – more and more people would want to buy the mangoes resulting in a higher demand.

Related: How digital payment methods are changing the face of the Indian economy

4. Inflation

Inflation refers to the ongoing change in the general level of prices in an economy. For an economy which is in a growing phase – like India’s economy – it is important to have a positive inflation. That is, over time the average price level of things must rise. Why is this so? Simple – this is the only scenario where investments will turn profits and you will want to make investments as the value of the money you hold goes down with time.

The problem with hyperinflation, inflation higher than 50% is that people cannot afford to buy anything and their basic needs may also go unfulfilled – think of Zimbabwe or Venezuela in recent years. On the other hand, negative inflation as experienced by Japan for an extended period halted the growth of the economy as there is no incentive to invest. Further, if you know that the price of things will fall further in the future – you will postpone all non-essential purchases resulting in a deadlock.

5. Trade deficit

Trade takes place not just between individuals within a nation – but also across borders. At its most basic, the two are no different – just a matching of demand and supply happening at a suitable price. But when a country spends more money on imports than it earns from its exports, it runs a trade deficit – also known as a current account deficit. The opposite happens when the exports outstrip the imports earning the country a trade surplus.

This is a natural outcome of trade and the underlying scarcity of resources. At no point in time can all countries have a trade surplus or vice-versa. Therefore, running a trade deficit is not bad in itself and should be evaluated in the light of other economic indicators of a nation. Read this beginner’s guide to capital markets.